Employment Situation for March 2014

By: Hope Wilkos, Writer/Blogger

March is now behind us and with April comes the promise of milder weather and a positive outlook on the job situation around the nation. Just as the employment statement was released, the Senate had decided the day before to move forward with the consideration of a bill to reinstate extended unemployment insurance. The President is also aggressively encouraging raising the minimum wage and passing the Paycheck Fairness Act.

There were a few significant points that came out of the statistics that were released on March employment. The private sector has added 8.9 million jobs over 49 straight months of job growth. Nonfarm payroll employment rose by 192,000 in the month of March. Government employment remained unchanged. Looking at only the last 12 months, private employment rose by 2.3 million which equates to 189,000 per month.

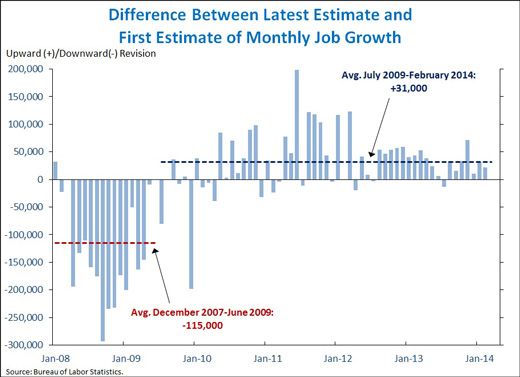

The estimate of job growth has been revised up in 18 of the last 19 months, and in 40 of the 56 months since the end of the recession in June of 2009. The reason for revisions is most commonly because the Bureau of Labor Statistics is missing data from firms that did not respond to the surveys in time, as well as data on business start-ups and closures. Keeping this in mind, January and February numbers were revised up by a combined 53,000 relative to the first report that was produced. Since June 2009, the latest data are an average of 31,000 per month higher than the first report which is an indication that recovery is stronger than initially estimated. However, during the recession from December 2007 to June 2009, first reports of monthly job growth were revised down by an average of 115,000 a month. This means that the recession was deeper than originally estimated.

If we concentrate on long-term unemployment and how to counteract that problem, we find that the long-term unemployed are a demographically diverse group and broadly similar to the shorter-term unemployed. It is not specific to any one occupation. This is an issue that must continue to be on the critical list to address in the best possible way.

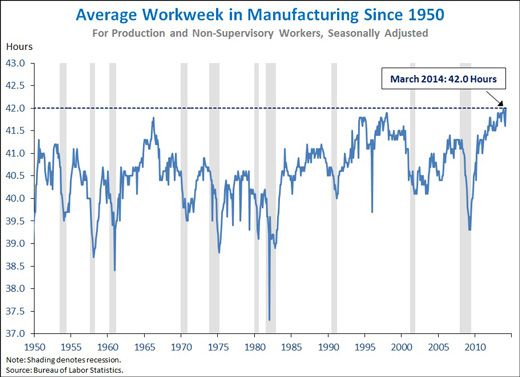

The average workweek in the manufacturing sector rebounded to 42.0 hours in March, tied for the highest since July of 1945. The average weekly hours for manufacturing production was at an all-time high in November of 2013 but then continued to edge downward from December of 2013 through February of 2014. The major reason for the decline is thought to be the unusually severe winter weather, including the major snowstorm that hit during the survey week in February. Consistent with the unwinding of weather effects, the average workweek in manufacturing jumped in March and returned to its 68-year high.

Lastly, employment gains in most industries in March were consistent with their range of monthly changes over the last several years. The construction sector had an above-average month, adding 19,000 jobs for a total of 88,000 over the past three months. In addition, state and local government performed relatively well, adding 9,000 jobs in March. Manufacturing employment was hardly changed, but with upward revisions in previous months, this sector has risen by 97,000 on net since last July.

Employer payrolls increased by 121,000 jobs in March, according to the Bureau of Labor Statistics’ establishment survey. The unemployment rate ticked down to 8.2% in March, according to the household survey. However, looking at this as a whole, employment was virtually unchanged in the household survey.

Indications highlight the continuing challenges facing construction workers, as a result of the collapse in homebuilding following the bursting of the housing bubble. The unemployment rate for construction workers stands at 17.2%, more than double the national average. Because of weak private sector demand for construction investment and the nation’s continuing need for improved infrastructure, including maintenance of existing highways, bridges, and ports, the President’s Budget proposal to increase and modernize the nation’s infrastructure is well targeted to support the economy today and in the future.

Other sectors with net job increases included leisure and hospitality (+39,000), professional and business services (+31,000), and financial activities (+15,000). Retail trade lost 33,800 jobs, construction lost 7,000 jobs, and government lost 1,000 jobs. State and local government job losses have moderated in recent months. Almost three-quarters of the slower job growth in March relative to February was due to slower growth in temporary help services and health care and day care services.

The outlook for the past six months has only given way to a brighter promise of reducing the overall unemployment and it remains to be seen how it continues to unfold for the remainder of the year.

STATEMENT ISSUED BY Jason Furman, Chairman of the Council of Economic Advisers. (Release from Office of the Press Secretary)

Comments are closed.