OCTOBER 2013 EMPLOYMENT SITUATION

By: Hope Wilkos, Writer/Blogger

This past week brought with it the once again anticipated results of the employment situation for October 2013. Although we had to contend with the government shutdown during the month of October, prior to the month we saw promising growth in August and September as well as solid third quarter GDP growth. October took a slight downturn due to the shutdown situation.

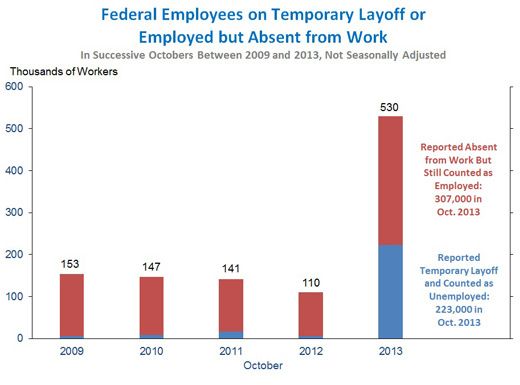

It appears that employment statistics dropped. Confusion entailed with some federal employees impacted by the shutdown counted as unemployed while others were counted as still employed. Only a portion of the roughly 400,000 furloughed federal employees were correctly counted as unemployed.

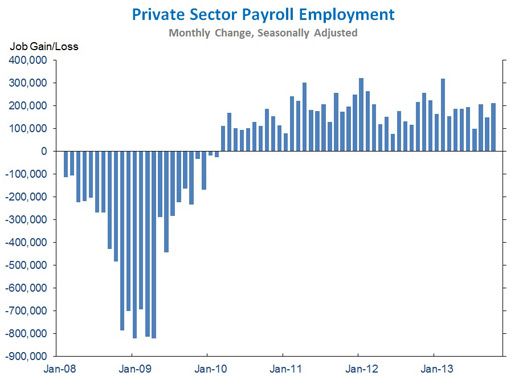

The resilient American businesses displayed more positive results with private sector employment increasing by 7.8 million over a period of 44 consecutive months. Total nonfarm payroll employment rose by 204,000 in October, due entirely to a 212,000 increase in private employment. Private sector job growth was revised up for August (to 207,000) and September (to 150,000) so that for the third quarter, private sector employment rose by an average of 152,000 per month (compared to the 129,000 per month average pace estimated in last month’s jobs report).

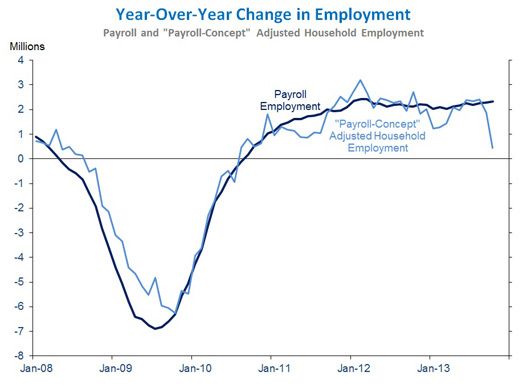

While nonfarm payroll employment rose by 204,000 in October, household survey employment fell by 735,000. The 939,000 gap between the two surveys is the largest since 1981 (excluding the effect of population control adjustments that can lead to outsize swings in the December-to-January change in the household survey). Until this month’s striking divergence, both surveys had told a similar story over a longer time horizon. As of September 2013, total nonfarm payrolls had risen 2.3 million over the preceding twelve months, while household survey employment (adjusted to be comparable to the concepts used in the establishment survey) rose by a similar 1.9 million. Although the October data disrupted this pattern, history suggests that both surveys will track each other over the long term.

Although we see construction beginning to pick up again, it remains 1.9 million jobs below its previous peak. However, this industry’s employment deserves some recognition as the month of October showed an increase of 11,000 jobs making the total rise to 185,000 over the last year (104,000 jobs in residential construction, 65,000 in non-residential construction and 16,000 in heavy and civil engineering construction). On Friday, November 8, 2013, President Obama set off to promote modernizing and investing in America’s ports and infrastructure with speeches given in New Orleans and then later in the day in Miami.

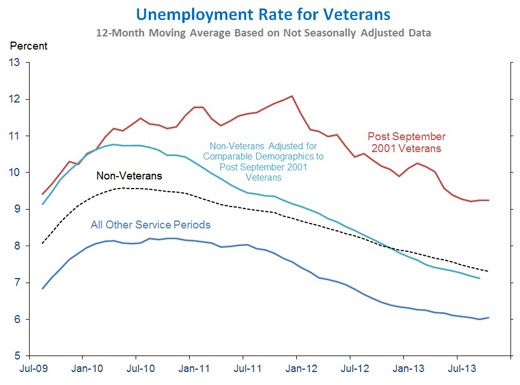

On Monday, November 11,2013, we mark Veteran’s Day and our veterans deserve a debt of gratitude for their brave efforts and outstanding service in the line of duty. We continue to try and put our vets back to work but the unemployment rate for post-9/11 veterans substantially increased higher than the unemployment rates for veterans of earlier periods and non-veterans. Directly comparing the employment situation of veterans from different service periods and non-veterans can be difficult because these groups differ substantially on characteristics that are correlated with employment and unemployment rates in the general population. Through the Joining Forces campaign led by First Lady Michelle Obama and Dr. Jill Biden, companies have already hired or trained 290,000 veterans and military spouses, with pledges to hire or train another 400,000 more. This Veterans Day, we must all reaffirm our commitment to serving those who have already served and sacrificed on our behalf.

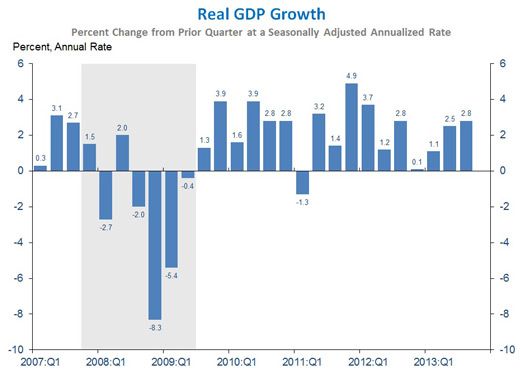

GDP Growth was boosted by a positive contribution for consumer durable purchases, continued recovery in the housing sector and net exports. The real gross domestic product climbed to 2.8% in the 3rd quarter as compared to 2.5% in the 2nd quarter.

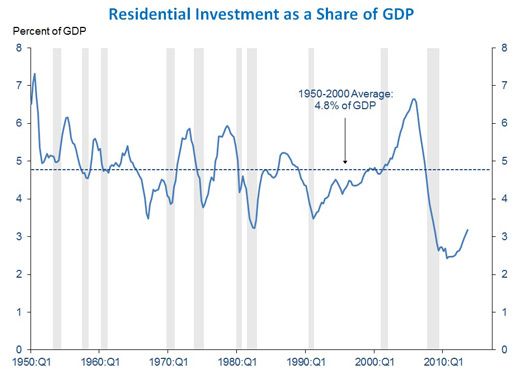

The private job sector had the greatest influence over the GDP growth. Export growth has returned in the Eurozone and is beginning to strengthen in other places also. Residential investment has posted double-digit annualized gains for five consecutive quarters. Housing investment plummeted during the financial crisis and remained weak early in the recovery, but has been growing strongly since the end of 2011. Despite the increase in mortgage rates this year, there is a significant upside potential in this sector, as housing investment remains well below its historic average as a share of the economy, while the pace of new housing starts, at about 900,000 homes annually, remains well below the pace implied by demographics.

We take the good with the bad and continue to try and improve the economic situation and promote job growth as we get ready to end 2013 and begin another year.

Statistics taken from release put out by Jason Furman, Chairman of the Council of Economic Advisers for the White House.

Comments are closed.